Master Policy vs Unit Owner Policy: The Gap Boards Miss

Last updated: May 26, 2026

Key Takeaway

An HOA master policy covers common areas and building structure, but it does NOT cover unit interiors, personal property, or owner improvements without the right master form. Every unit owner needs an HO-6 policy to fill the gap — and every board needs to know which master form (bare walls-in, single entity, or all-in) is in force because it determines exactly where the HOA's coverage ends and the owner's begins. The boards that get blindsided at the annual meeting are the ones that never disclosed the form.

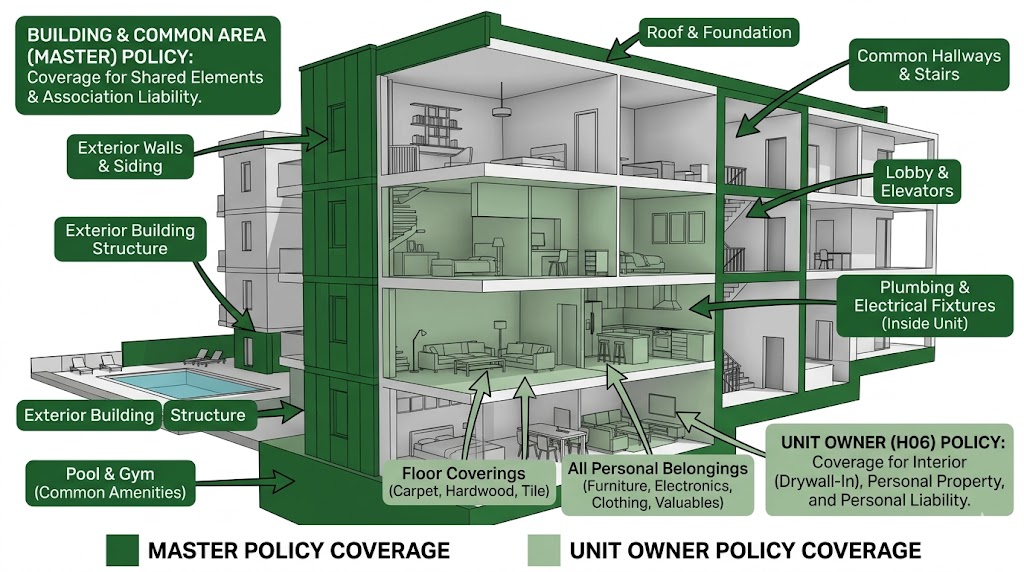

What is the difference between an HOA master policy and a unit owner policy?

An HOA master policy covers the building structure, common areas, and shared amenities. A unit owner (HO-6) policy covers the interior of the unit, personal property, improvements, and personal liability. The gap between these two policies is where most disputes — and special assessments — happen, and the gap is defined by which of three master forms the association carries: bare walls-in, single entity, or all-in. Boards that haven't confirmed their form in writing are the ones that get blindsided when a loss hits.

FOR HOA BOARDS

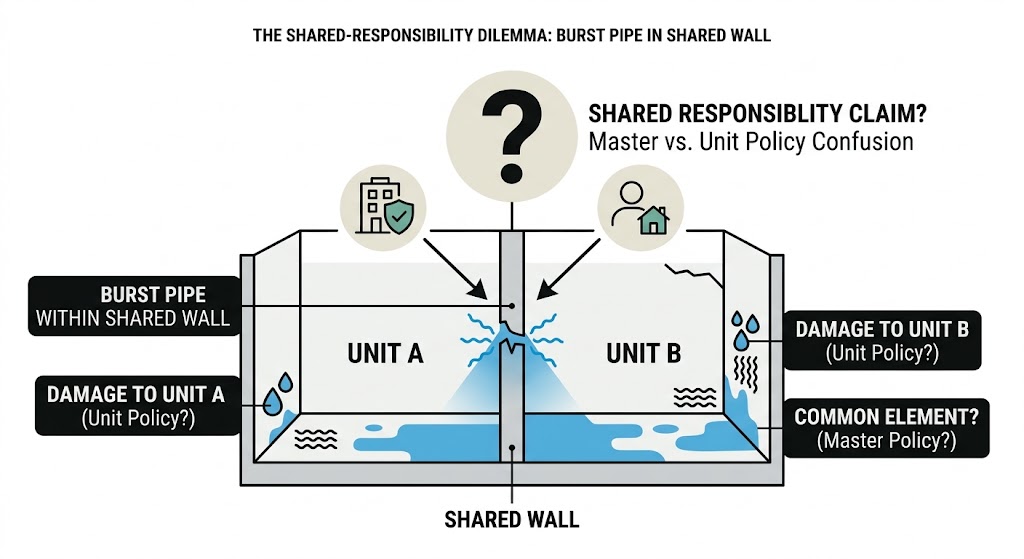

A pipe bursts. Whose insurance pays?

When water damage hits a unit, the master policy and the unit owner's HO-6 carriers point at each other. The board assumes the master handles it. The homeowners assume their HO-6 handles it. Neither is fully right — and the gap between what each policy actually covers is the single biggest source of HOA insurance disputes at annual meetings. The conversation most boards don't have isn't about which policy is bigger. It's about which master form is in force, what the HO-6 has to fill, and whether the membership knows the boundary before the next loss makes everyone find out the hard way.

A Pipe Bursts. Whose Insurance Pays?

When water damage hits a unit, the master policy and the unit owner's HO-6 carriers point at each other. The board assumes the master handles it. The homeowners assume their HO-6 handles it. Neither is fully right — and the gap between what each policy actually covers is the single biggest source of HOA insurance disputes at annual meetings. The conversation most boards don't have isn't about which policy is bigger. It's about which master form is in force, what the HO-6 has to fill, and whether the membership knows the boundary before the next loss makes everyone find out the hard way.

The HOA master policy is a commercial insurance policy the association purchases to cover the shared property the HOA is responsible for maintaining — building structure, common areas, shared amenities, building systems. The HO-6 is what unit owners buy to cover what the master policy doesn't. The boundary between the two is defined by three distinct master policy forms. Boards that haven't confirmed which form is in force often discover the gap only when a claim arrives. For the broader HOA insurance program context, see our HOA insurance cost breakdown; for the D&O exposure that runs in parallel, see D&O insurance for HOA board members.

373K+

U.S. community associations as of 2025 — the universe where master-vs-HO-6 boundary disputes happen every day across the country

Foundation for Community Association Research, 2025 Statistical Review

78.1M

residents living in U.S. community associations — every unit owner depending on the master/HO-6 boundary their board may not have disclosed

Foundation for Community Association Research, 2025 Statistical Review

$12.9T

property value held inside U.S. community associations as of 2024 — the replacement cost exposure boards underwrite via the master form choice

Foundation for Community Association Research, 2024 industry data

The Three Master Policy Forms

Not all master policies are created equal. Three forms exist, and the form your HOA carries determines exactly where the association's coverage ends and the unit owner's HO-6 begins. The card grid below maps each form's coverage scope and what the HO-6 has to fill.

01

🧱Bare Walls-In

Most limited form. The master covers structure only — exterior walls, roof, floors, building systems, common areas. Nothing inside the units. Drywall, paint, original fixtures, flooring, cabinets — all of it falls to the HO-6. Typically matches older condo CC&Rs and cost-conscious associations. The HO-6 has to fill the most ground.

02

🏗️Single Entity

Middle ground. The master covers structure plus original fixtures and finishes as installed at the time of construction or original sale. Original drywall, original carpet, original cabinets — all in. But owner upgrades and improvements made after purchase are not. The HO-6 fills upgrades and personal property. Matches most modern condo CC&Rs.

03

🏛️All-In (Comprehensive)

Broadest form. The master covers structure, original fixtures, AND owner improvements and upgrades. A remodeled kitchen is covered under the master. These policies cost more, but they dramatically narrow the HO-6's scope to personal property, additional living expenses, and personal liability. Matches newer construction and premium-tier communities.

The HO-6 fills whatever the master form leaves uncovered. A good HO-6 includes dwelling coverage for the interior elements the master doesn't carry, personal property coverage for furniture and belongings, personal liability if someone is injured in the unit, additional living expenses during repairs, and — the line most owners overlook — loss assessment coverage. Standard HO-6 policies include $1,000 in loss assessment coverage; on a meaningful loss that exceeds the master policy limit, that minimum exhausts immediately. Use our HOA insurance risk calculator to see what your association's structure should be carrying at the master level.

Master Policy Coverage Boundary by Form Type

The table below maps coverage element by master form against dispute frequency. The cells flag which boundaries cause the most disputes at annual meetings — the ones where boards take the most heat when owners discover the gap after a loss.

Coverage Boundary

Master Policy Coverage Boundary by Form Type

The three master forms divide responsibility between the association and the unit owner very differently. The grid below maps the boundary by form and flags which boundaries cause the most disputes when a loss surfaces them.

| Rating Factor | Impact on Premium | |

|---|---|---|

| Roof, exterior walls, foundation | MinorAll three forms: Covered. Master policy core scope. | |

| Common areas (lobbies, hallways, elevators) | MinorAll three forms: Covered. HOA-maintained common scope. | |

| Shared amenities (pool, clubhouse, gym) | MinorAll three forms: Covered. Association property. | |

| Building systems (plumbing mains, electrical panels, HVAC) | MinorAll three forms: Covered. HOA maintenance scope. | |

| Interior drywall and paint | CriticalBare walls: HO-6 fills. Single entity: master covers if original. All-in: master covers. | |

| Original fixtures (cabinets, countertops, flooring as built) | SignificantBare walls: HO-6 fills. Single entity: master covers. All-in: master covers. | |

| Owner upgrades and improvements | CriticalBare walls: HO-6 fills. Single entity: HO-6 fills. All-in: master covers. | |

| Personal property (furniture, electronics, belongings) | NotableAll three forms: HO-6 fills. Never on the master. | |

| Personal liability (injury in the unit) | NotableAll three forms: HO-6 fills. Master GL is for common areas. | |

| Additional living expenses during repairs | NotableAll three forms: HO-6 fills. Master doesn't carry it. | |

| Loss assessment after a master-policy-exceeding loss | CriticalAll three forms: HO-6 fills. Standard HO-6 minimum is $1,000 — usually inadequate. |

The pattern: bare walls-in puts the most responsibility on the HO-6; all-in puts the most on the master. The form most boards never disclose is the form most owners need to know to size their HO-6 correctly — and the gap, when it surfaces, is what turns next year's election into a referendum.

A few notes on how to read the table. Interior drywall and original fixtures are the boundary lines most boards never disclose in writing — those are the boundaries that turn a routine claim into an annual meeting referendum. Owner upgrades are uniformly excluded from bare-walls-in policies; the only master form that catches them is all-in. And the loss assessment line at the bottom is the HO-6's job in every scenario — the master policy doesn't carry it because special assessments are by definition a member-level expense.

Before the next renewal

Most HOA boards never confirm which master policy form they actually carry.

We pull your declarations, confirm whether the form is bare walls-in, single entity, or all-in, and walk through what every unit owner's HO-6 actually needs to fill — before the next loss surfaces the gap.

“Most HOAs carry bare walls-in policies, which means unit owners carry the most responsibility. If the board doesn't know which form the association has, that's the first thing to find out.”

— Bobby Friel · Partner, Direct Insurance Services

The Special Assessment Trap

The scenario most boards underestimate: a major fire or water event causes damage that exceeds the master policy property limit. The HOA is now short on the rebuild — and the shortfall gets divided among all unit owners as a special assessment. In a 50-unit building with a $1 million shortfall, that's $20,000 per owner. If owners don't have adequate loss assessment coverage on their HO-6 policies, they're paying that out of pocket. We've seen boards in Texas and Colorado face exactly this situation, and it creates financial hardship for owners and legal liability for the board.

The fix is two-fold. First, make sure the master policy limits are adequate for the actual replacement cost of the building — not the market value, the replacement cost. A building built for $5 million ten years ago might cost $8 million to rebuild today. Second, require all unit owners to carry HO-6 policies with meaningful loss assessment limits. We recommend $50,000 minimum for most communities, and for high-rise buildings in expensive markets, $100,000 is better. Many CC&Rs allow the board to mandate this; if yours don't, it's worth amending them. In California, the Davis-Stirling Act requires HOAs to distribute an annual insurance disclosure to owners that explains what the master policy covers and recommends owners purchase HO-6 coverage. Even if your state doesn't require this, it's a best practice every board should follow.

Boards That Assume vs. Boards That Verify

The boards that get blindsided at the annual meeting are the ones that never confirmed the master form in writing. The boards that don't are running a disciplined review every renewal cycle. Five places where that discipline shows up:

Boards That Assume the Master Covers Everything

- ×Master form never confirmed against the CC&Rs

- ×Annual owner disclosure of master form / HO-6 expectations not done

- ×Replacement cost values stale (last appraisal 5+ years old)

- ×Loss assessment limits in CC&Rs amendments never reviewed

- ×Special assessment after a loss surprises everyone at the annual meeting

Boards That Verify Before the Next Loss

- ✓Master form confirmed annually against the CC&Rs

- ✓Annual owner disclosure of master form + HO-6 expectations documented

- ✓Replacement cost appraisal on a 2-3 year cadence

- ✓Loss assessment limits documented in CC&Rs amendments

- ✓Coverage boundary explained at the annual meeting before someone needs to ask

HOA Scenario

OPERATOR SCENARIO

Scenario

Imagine you're at the annual meeting, two months after a third-floor pipe burst flooded units below. The master policy paid for the structural rebuild. Four unit owners just realized their HO-6 carriers won't cover the interior damage because the master policy your board carries is bare-walls-in, not all-in — and nobody told them which form was in force.

What we did

What changes for the homeowner trust you spent years building when four families find out at the annual meeting that the coverage gap was the board's to disclose, not theirs to discover?

🎯 The Outcome

Could the master policy form that's been on autopilot for the last five renewals already be the gap that turns next year's election into a referendum on the current board?

FAQ

How do we figure out which master policy form our association actually carries?

The master policy declarations page (the front of the policy document) will name the coverage form. Look for language like "bare walls coverage," "single entity," "all-in," or "comprehensive." If the dec page isn't clear, the policy's coverage form code (typically an ISO form number) will identify it. Boards that have rolled the same policy forward through multiple renewals without reviewing it sometimes don't know which form is in force — pulling the declarations and confirming is the first step of any master policy review.

Do unit owners need a different HO-6 depending on which master form is in force?

Yes, materially. Under a bare-walls-in master, the HO-6 must carry dwelling coverage that includes all interior finishes (drywall, paint, flooring, fixtures, cabinets). Under a single-entity master, the HO-6 fills upgrades and personal property only. Under an all-in master, the HO-6 narrows to personal property, additional living expenses, and personal liability. The HO-6 limit and the dwelling-coverage component should be calibrated against the actual master form — owners under a bare-walls-in master who carry an HO-6 sized for an all-in master will be materially underinsured if they file a claim.

What's loss assessment coverage on an HO-6 and why does it matter?

Loss assessment coverage on the HO-6 pays the unit owner's share of a special assessment levied by the HOA after a covered loss that exceeds the master policy limits. Standard HO-6 policies include $1,000 in loss assessment coverage as a baseline — that minimum is almost always insufficient on a meaningful loss. We recommend $50,000 minimum for most communities and $100,000 for high-rise or expensive-market communities. The cost difference between $1,000 and $50,000 of loss assessment coverage is typically modest on the annual HO-6 premium.

If the master policy doesn't cover something the CC&Rs say it should, who's responsible?

Boards are responsible for procuring insurance that matches what the governing documents require. When the master policy doesn't carry what the CC&Rs call for, the board has both a coverage gap and a governance gap — a D&O claim from an aggrieved homeowner is one of the predictable consequences. The annual master policy review should include a CC&Rs compliance check: pull the insurance requirements section of the governing documents and confirm the current master policy carries everything called for. This is the conversation we run with every HOA board we review.

The Bottom Line

The master policy and the HO-6 are designed to work together — but only if the board knows which master form is in force and discloses it to every unit owner. The gap between what each policy covers is where annual meetings turn into special assessments, and special assessments turn into board elections.

For the broader HOA insurance program — master property, GL, D&O, and fidelity bond — read our HOA insurance cost breakdown. For the parallel governance liability that runs alongside the master policy review, see D&O insurance for HOA board members. The HOA Board Insurance Guide covers the full four-policy program every association carries.

If your HOA hires contractors for maintenance or renovation work, make sure they carry proper contractor insurance with the HOA named as additional insured. For mixed-use properties that include rental units, building owner coverage for the rental portion may also apply. If your association needs help funding a special assessment or capital improvement, HOA reserve financing and association loans can bridge the gap. And for state-specific HOA insurance requirements, check our state commercial insurance guides — rules vary significantly between states like Arizona and California.

The board's job is to protect the association — and that starts with understanding exactly where your insurance coverage begins and ends. Use our HOA insurance risk calculator to see where the factors land, then we'll review your current master policy and walk through the gaps against the CC&Rs before the next renewal lands.

The board member's question

Not "which policy is bigger." The right question is "which master form is in force, what does the HO-6 have to fill, and does every unit owner know the boundary before the next loss makes them find out the hard way?" The coverage gap is the board's to disclose. The annual meeting is the worst time for the membership to discover it.

About the Author

Bobby Friel

Partner, Direct Insurance Services

Bobby Friel is a partner at Direct Insurance Services, where Patrick Henigan and the licensed team handle all quoting, policy reviews, and binding. Bobby runs the commercial division's marketing, content, and client outreach — helping contractors, HOA boards, restaurant owners, and commercial landlords across 29 states find the right coverage through Insurance Service 365.

Related Coverage

Explore Related Coverage Options

🏢 The Complete HOA Insurance Guide 2026

What every HOA board member needs to know about master policies, D&O coverage, fidelity bonds, and the coverage gaps that cost associations hundreds of thousands of dollars.

Read the Free Guide →

Ready When You Are

Ready When You Are

No pressure. No obligation. Just real quotes from 30+ carriers, reviewed on video so you understand exactly what you're buying.

Takes ~2 minutes · Contract review included · Video walkthrough on every option