Commercial Landlord Insurance: What Owner Policies Skip

Last updated: May 26, 2026

Key Takeaway

Commercial landlord insurance is purpose-built for landlords who lease space to tenants. It covers the building, common areas, premises liability, and lost rental income. Your tenant's insurance does NOT protect you as the building owner — and a standard commercial property policy was built for owner-occupied businesses, not tenant-occupied buildings. The conversation worth having before the next renewal is whether the form your carrier writes actually matches the operation.

What is commercial landlord insurance?

Commercial landlord insurance (sometimes called lessor's risk in technical/policy-form context) is a commercial policy designed for landlords who lease property to tenants. It covers the building structure, common areas, premises liability for shared spaces, and loss of rental income when a tenant space goes offline. Unlike standard commercial property insurance — which was built for owner-occupied businesses — it's specifically structured for the risks of non-owner-occupied commercial buildings.

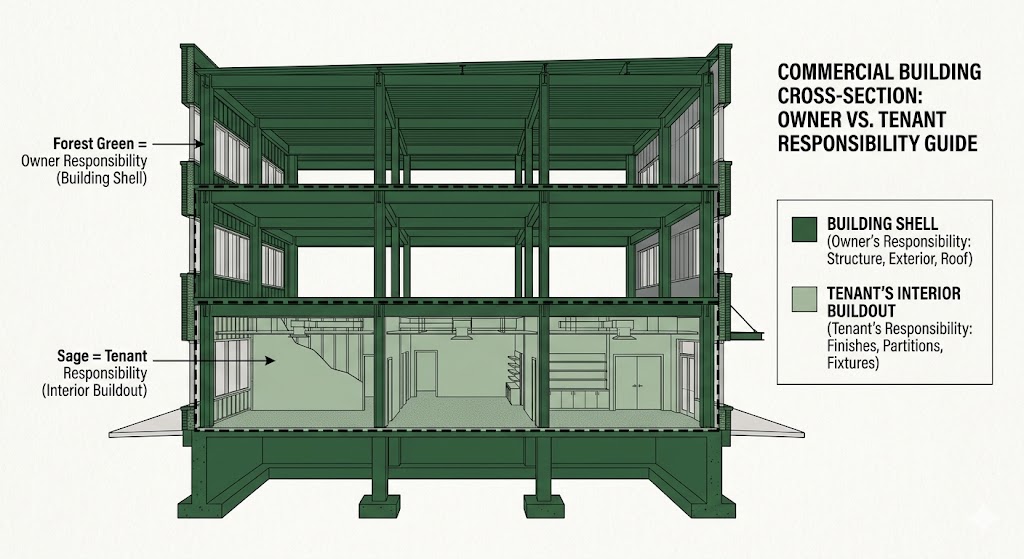

FOR BUILDING OWNERS

Your tenant's lease protects your legal rights. Their insurance protects them.

Commercial landlords inherit risk from their tenants that owner-occupied property policies were never designed to handle. Vacancy exposure, premises liability for common areas, loss of rents when tenant space goes dark, building limit drift across renewals — none of these are addressed by a standard commercial property policy. The conversation worth having before the next renewal isn't about price. It's about whether the form your carrier writes was built for an owner-occupied business or a tenant-occupied building.

The Lease Protects Your Rights. The Insurance Protects Your Position.

Commercial landlords inherit risk from their tenants that owner-occupied property policies were never designed to handle. Vacancy exposure, premises liability for common areas, loss of rents when a tenant space goes dark, building limit drift across renewals — none of these are addressed by a standard commercial property policy. The conversation worth having before the next renewal isn't about price. It's about whether the form your carrier writes was built for an owner-occupied business or a tenant-occupied building.

Commercial landlord insurance — sometimes called lessor's risk in technical/policy-form context — exists for exactly this situation: when you own the building but someone else operates a business inside it. For the parallel cash-flow exposure, see loss of rents coverage for landlords. For the broader commercial real estate insurance picture, the Landlord Insurance Gaps Guide covers the coverage pitfalls we see across the building owners we review.

5.9M

U.S. non-residential buildings — the universe of commercial properties where landlord vs owner-occupied policy form decisions matter every renewal

U.S. Energy Information Administration / CBECS, 2018 (most recent comprehensive non-residential building stock survey)

97%

share of U.S. commercial building stock under 100,000 square feet — the small-and-mid commercial property universe where standard owner-occupied policy forms most often get misapplied to tenant-occupied buildings

U.S. Energy Information Administration / CBECS commercial building stock data

7%

increase in U.S. nonresidential building construction put in place through Sept 2024 vs same period 2023 — replacement cost escalation that building limits often haven't kept pace with

U.S. Census Bureau Construction Spending, September 2024

What Commercial Landlord Insurance Actually Covers

Commercial landlord insurance — sometimes called lessor's risk in technical terms — is a commercial policy designed specifically for landlords who lease property to tenants. The form covers the lessor's risk (the landlord's risk), not the tenant's risk. It's a distinct product from a standard commercial property policy, and the distinction shows up at claim time.

The card grid below maps the lines every commercial landlord program carries.

01

🏢Building Coverage

Replacement cost coverage for the physical structure — walls, roof, foundation, permanent fixtures, building systems (HVAC, plumbing, electrical). The insurer pays to rebuild or repair at current construction costs. Building limits that haven't been reviewed against rebuild values in years are where most underinsurance gaps surface.

02

⚖️Premises Liability

Coverage when someone is injured on the property in an area the landlord is responsible for — common areas, parking lots, building exterior, shared amenities. Delivery driver slips on ice in the parking lot, visitor injured on common-area stairs — these are landlord exposures, not tenant exposures.

03

💵Loss of Rents

Replaces rental income when a covered loss makes a tenant space uninhabitable during repairs. Typically set to 12 months of gross rent at the time of bind. The limit drifts out of alignment with rent increases between renewals — boards that don't review it discover the gap at claim time.

04

🌂Commercial Umbrella

Excess liability stacked above the primary landlord policy and any commercial auto. Activated when underlying limits exhaust. Premises liability verdicts on common-area injuries can exceed seven figures; landlords with public-facing tenants or multiple properties typically need umbrella layered.

05

🚫Vacancy Endorsement

Modifies the standard vacancy exclusion that triggers when a building has been vacant for more than 60 consecutive days or more than 31% of square footage is unoccupied. Without the endorsement, vandalism, water damage, theft, and sprinkler leakage get excluded entirely during the vacancy period.

When a tenant space goes offline, the rental income vanishes but the mortgage doesn't pause. The longer the repair cycle, the bigger the cash-flow hole. Loss of rents is the line item that bridges that gap — and the limit most landlords set wrong the first time. For a deeper read on that specific exposure, see loss of rents coverage for landlords.

Why Your Tenant's Insurance Isn't Enough

Every good commercial lease requires tenants to carry their own insurance. What most landlords don't fully appreciate: your tenant's policy protects the tenant, not you. A tenant's GL policy covers claims arising from the tenant's operations inside their leased space. It doesn't cover the building structure. It doesn't cover common areas. And it doesn't cover your lost rental income.

Even if your lease requires the tenant to name you as an additional insured on their policy — which it should — that endorsement only extends the tenant's liability coverage to you for claims arising from the tenant's operations. It doesn't replace your need for your own building coverage, your own liability coverage for common areas, or your own loss of rents protection. We've seen landlords with ironclad leases still end up personally exposed because they assumed their tenant's insurance was enough.

There's also the practical problem of tenant compliance. Tenants are required to maintain insurance under the lease, but policies lapse, get cancelled, or don't meet the lease requirements. If your tenant's insurance isn't in force when a loss occurs, their lack of coverage becomes your problem. Your commercial landlord policy is the backstop.

“Landlords with ironclad leases still end up personally exposed when they don't carry the right building owner policy. The lease protects your legal rights. The policy protects your financial position.”

— Bobby Friel · Partner, Direct Insurance Services

What Drives Your Commercial Landlord Insurance Premium

Commercial landlord insurance premiums are rated against a defined set of factors — building type, tenant mix, claims history, vacancy posture, replacement cost adequacy, and the rest of the grid below. Two similar-looking buildings can rate very differently depending on which factors land harder.

Premium Drivers

What Drives Your Commercial Landlord Insurance Premium

Commercial landlord insurance premiums are rated against a defined set of factors specific to non-owner-occupied buildings. Here's what underwriters actually evaluate.

| Rating Factor | Impact on Premium | |

|---|---|---|

| Building type and occupancy use | SignificantOffice, retail, industrial, mixed-use each rate differently | |

| Single tenant vs multi-tenant | SignificantMulti-tenant exposure layers premises liability and tenant-mix risk | |

| Tenant credit profile and industry mix | SignificantRestaurant tenant vs professional services vs retail all rate differently | |

| Building age and construction class | SignificantFrame vs masonry, older systems vs current code | |

| Location (coastal, flood zone, high-crime) | CriticalGeographic risk overlay can dominate every other factor | |

| Vacancy history | Significant60-day vacancy provision triggers fast on policies without endorsement | |

| Lease terms (triple-net vs gross) | NotableLease structure determines who carries which insurance line | |

| Deferred maintenance posture | NotableOld roof, outdated electrical narrow carrier appetite | |

| Replacement cost adequacy | SignificantBuilding limits often haven't kept pace with rebuild cost escalation | |

| Loss runs (last 5 years) | CriticalPrior claims drive renewal pricing; multi-claim runs narrow appetite |

No single factor decides the premium. The combination — and especially how the tenant mix interacts with the building age and the replacement cost adequacy — is what determines whether the renewal matches what the operation actually requires.

A few notes on how to read the table. Tenant credit profile and tenant industry mix drive premium more than most landlords realize — a building with a restaurant tenant and a nail salon prices differently than the same building with two professional-services tenants. Vacancy history matters because the standard vacancy provision triggers fast (see below). Replacement cost adequacy matters because property values escalate but building limits often don't — buildings built for one cost a decade ago may rebuild for materially more today.

Before the next renewal

Most commercial landlords don't realize their property policy was built for owner-occupied businesses, not tenant-occupied buildings.

We review your current building policy, confirm the lessor's-risk-specific endorsements are in place, and walk through what changes when a tenant vacates or a claim hits.

Standard Commercial Property vs. Commercial Landlord Insurance

The single most consequential decision on a building owner's insurance program is whether the carrier writes the policy on a standard commercial property form (owner-occupied default) or a commercial landlord form (purpose-built for tenant-occupied buildings). Five places where that choice shows up:

Standard Commercial Property Policy

- ×Owner-occupied policy form by default

- ×No premises liability for common areas

- ×No loss of rents coverage

- ×Vacancy provision triggers fast (no endorsement layered)

- ×Tenant operations create unintended coverage gaps

Commercial Landlord Insurance

- ✓Purpose-built for non-owner-occupied buildings

- ✓Premises liability for common areas

- ✓Loss of rents at 12-month limit

- ✓Vacancy endorsement available when needed

- ✓Tenant operations underwritten properly at bind

Building Owner Scenario

OPERATOR SCENARIO

Scenario

Imagine you own a small strip mall and a tenant's kitchen fire causes structural damage plus smoke damage to two adjacent units. The contractor estimates a four-month rebuild. Your tenants need to move out. The mortgage payment is still due on the first of every month.

What we did

What changes for you if the property policy your prior agent placed was built for owner-occupied buildings and your loss-of-rents limit hasn't been reviewed against current rent rolls in three years?

🎯 The Outcome

Could the policy that's been on autopilot through the last two renewals already be the gap that turns a four-month rebuild into a personal cash-flow crisis?

The Vacancy Exclusion Trap

Most commercial property policies — including commercial landlord forms — contain a vacancy exclusion that modifies coverage when a building has been vacant for more than 60 consecutive days. If more than 31% of the building's total square footage is unoccupied, the vacancy provision kicks in.

Under the standard vacancy exclusion, certain causes of loss are excluded entirely — vandalism, sprinkler leakage, building glass breakage, water damage, and theft. For covered losses that still apply, the insurer typically reduces the claim payment by a meaningful percentage. When the building is underinsured or partially vacant, coinsurance penalties can leave you covering a meaningful share of a covered loss out of pocket.

This matters because commercial buildings do go vacant — tenants move out, leases expire, spaces take months to re-lease. When a significant portion of your building will be unoccupied, the vacancy endorsement is the conversation worth having with the agent before the 60-day clock starts. Review our Landlord Insurance Gaps Guide for more coverage pitfalls like this one.

FAQ

What's the difference between lessor's risk insurance and a standard commercial property policy?

Lessor's risk is the policy form name (and the technical term carriers use); commercial landlord insurance is what we call it in plain language. The form is purpose-built for non-owner-occupied buildings — premises liability for common areas, loss of rents during covered repair cycles, tenant-mix underwriting, vacancy endorsements available. A standard commercial property policy is built for owner-occupied businesses; when a landlord runs it through a property they don't occupy, the gaps show up at claim time.

Does my tenant's policy actually protect me as the building owner?

No. The tenant's policy covers claims arising from the tenant's operations — claims for the tenant, not the building. Additional insured status on the tenant's policy extends the tenant's liability to the landlord for claims arising from the tenant's operations, but it doesn't cover the building structure, common areas, or your lost rental income. The landlord needs the landlord's own policy. The tenant's policy is supplemental, not primary.

What is a vacancy exclusion and how do I avoid getting caught by it?

The vacancy exclusion is a standard provision in most commercial property forms — including commercial landlord forms — that limits coverage when a building has been vacant for more than 60 consecutive days or when more than 31% of the building's total square footage is unoccupied. Vandalism, water damage, theft, and sprinkler leakage get excluded entirely; other covered losses get reduced. The fix is a vacancy endorsement or short-term vacant building coverage, layered before the 60-day clock runs out.

When do I need a commercial umbrella on top of my building policy?

Single-tenant office buildings with limited foot traffic typically don't need it. Strip malls, mixed-use buildings, restaurant-tenant buildings, and any property with significant public foot traffic typically do. Premises liability verdicts on common-area injuries can exceed seven figures; when the verdict exceeds the underlying landlord policy's liability limit, the excess comes out of personal assets unless an umbrella is layered above. Every landlord with more than one property — or any property with public-facing tenants — should carry at least $1 million in umbrella coverage.

The Bottom Line

Commercial landlord insurance isn't a different policy from your tenant's — it's a different policy from the one most agents write by default for property owners. The conversation worth having before the next renewal isn't about what it costs. It's about whether the form your carrier writes was built for an owner-occupied business or a tenant-occupied building.

For the parallel cash-flow exposure, see loss of rents coverage for landlords. State-specific rate structures differ — properties in California, Colorado, and Texas price against different filings. When hiring contractors for repairs or tenant improvements, verify they carry contractor insurance with your property named as additional insured. For mixed-use development with a homeowners association, the HOA may carry a master policy for shared structures, but your individual units still need their own commercial landlord insurance. And if you're acquiring new properties or refinancing, commercial real estate financing and property loans can help you move fast.

The fastest way to find out where your current setup stands? Use our commercial landlord risk calculator to see where the factors land, then we'll review your current building policy and walk through the gaps against your tenant mix and lease terms before the next renewal.

The building owner's question

Not "what does landlord insurance cost." The right question is "is the policy form my carrier wrote against this property actually a commercial landlord form, or is it a standard commercial property form that's been quietly mismatched to a tenant-occupied building?" The form decision shows up at claim time, not at renewal.

About the Author

Bobby Friel

Partner, Direct Insurance Services

Bobby Friel is a partner at Direct Insurance Services, where Patrick Henigan and the licensed team handle all quoting, policy reviews, and binding. Bobby runs the commercial division's marketing, content, and client outreach — helping contractors, HOA boards, restaurant owners, and commercial landlords across 29 states find the right coverage through Insurance Service 365.

Related Coverage

Explore Related Coverage Options

🏠 The Complete Commercial Landlord Insurance Guide 2026

What every building owner needs to know about lessors risk, loss of rents, vacancy exclusions, and the coverage gaps that leave landlords exposed.

Read the Free Guide →

Ready When You Are

Ready When You Are

No pressure. No obligation. Just real quotes from 30+ carriers, reviewed on video so you understand exactly what you're buying.

Takes ~2 minutes · Contract review included · Video walkthrough on every option