Loss of Rents Coverage: The Cash Flow Gap Landlords Miss

Last updated: May 26, 2026

Key Takeaway

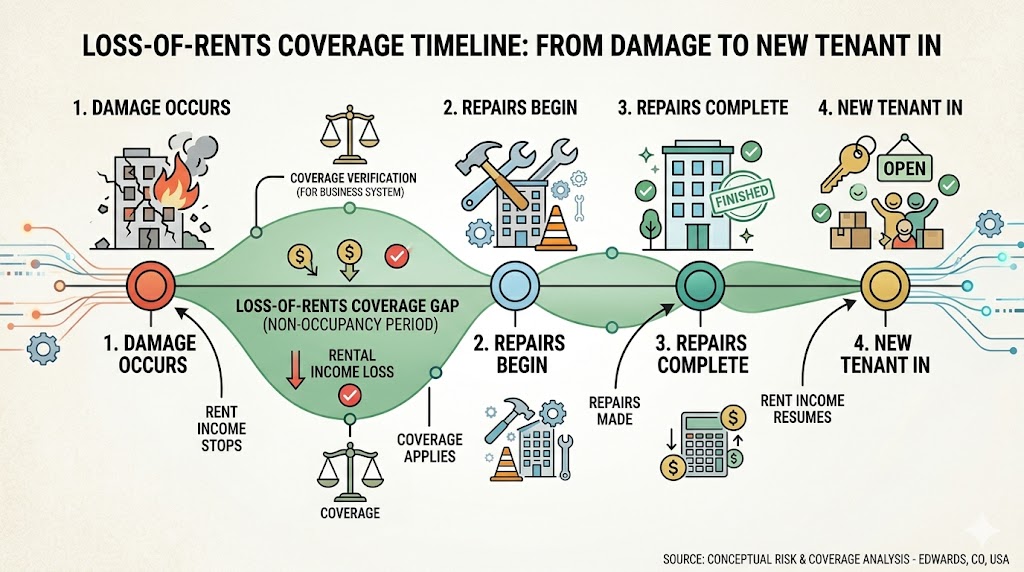

Loss of rents coverage is the line item that bridges the gap between a covered loss and the mortgage payment that's still due — and the limit most landlords set wrong the first time. It reimburses your rental income when a tenant space goes unoccupiable due to a covered loss, typically up to 12 months. Most policies are bound against rents that haven't been raised in years. When the loss hits, the gap shows up in cash flow before it shows up anywhere else.

What is loss of rents coverage for landlords?

Loss of rents coverage (also called rental income coverage or business income coverage on a commercial landlord policy) reimburses you for lost rental income when a covered event — like a fire, storm, or burst pipe — makes a tenant space unoccupiable. It covers the rental income you would have collected during the repair period, usually up to 12 months of gross rent. The limit is typically set against rents at the time of bind — if rents have increased and the limit hasn't been reviewed, the gap surfaces at claim time.

FOR BUILDING OWNERS

Tenant space goes dark. The mortgage doesn't pause.

When a covered loss takes a tenant offline, the building is being rebuilt but the mortgage payment is still due on the first of every month. Loss of rents is the line item that bridges that gap — and the limit most landlords set wrong the first time and never review again. Most policies are bound against rents that haven't been raised in years. When the loss hits, the gap shows up in cash flow before it shows up anywhere else.

The Cash-Flow Gap

When a covered loss takes a tenant offline, the building gets rebuilt but the mortgage payment is still due on the first of every month. Property taxes don't pause. Insurance doesn't pause. The income that was supposed to cover those expenses just vanished for the length of the repair cycle. Loss of rents is the line item that bridges that gap — and the limit most landlords set wrong the first time and never review again.

The pattern shows up across the commercial landlords we review: a policy bound years ago against rents that haven't been raised, a limit that covers 4-6 months on a repair cycle that runs 7-12, a vacancy gap unaddressed, tenant business income confused with landlord rental income. When the loss hits, the gap shows up in cash flow before it shows up anywhere else. For the broader commercial landlord insurance picture and what every building owner program carries, see our guide on commercial landlord insurance and the building owner gap.

5.9M

U.S. non-residential buildings — the universe of commercial properties where loss-of-rents limit adequacy is the line item that decides cash flow at the moment of loss

U.S. Energy Information Administration / CBECS commercial building stock data

7%

increase in U.S. nonresidential building construction put in place through Sept 2024 vs same period 2023 — rebuild cost escalation that drives repair-cycle duration and loss-of-rents limit adequacy

U.S. Census Bureau Construction Spending, September 2024

97%

share of U.S. commercial building stock under 100,000 square feet — the small-and-mid commercial property universe where loss-of-rents limits drift hardest between renewals

U.S. Energy Information Administration / CBECS commercial building stock data

What Loss of Rents Actually Pays For

Loss of rents coverage — sometimes called rental income coverage or business income coverage on a commercial landlord policy — reimburses you for the rental income you lose when a covered event makes a tenant space unoccupiable. The card grid below maps the four covered triggers.

01

🔥Fire and Smoke Damage

The most common trigger. Whether it's a kitchen fire, electrical fire, or arson, if the space can't be occupied during repairs, your lost rent is covered up to the policy limit. Restaurant-tenant buildings see the highest fire-driven loss-of-rents activity.

02

💧Water Damage

Burst pipes during winter freezes, roof leaks during storms, sprinkler system malfunctions, or accidental discharge — anything that makes a space unusable while repairs run. Multi-floor commercial buildings see water-driven losses cascade across multiple units.

03

🌪️Wind and Hail Damage

Severe storms that damage the roof or structure enough to require the tenant to vacate during repairs. In coastal and tornado-belt markets, this is the most consequential single-loss-event category for loss-of-rents.

04

🚨Vandalism

Break-ins, vandalism, or willful damage that renders the space unoccupiable during the repair window. Lower frequency than fire and water but legitimate covered cause-of-loss on most commercial landlord forms.

What it doesn't cover: a tenant who just stops paying rent (that's an eviction issue, not an insurance issue), or damage caused by the tenant themselves (that's typically on their renter's insurance or commercial policy). The coverage limit is usually set at 12 months of gross rental income; the waiting period is typically 72 hours after the covered event. For losses lasting longer than a week or two, that 72-hour deductible is negligible.

What Drives Your Loss of Rents Limit Adequacy

The premium is small. The limit-adequacy question is the one that actually decides whether the policy responds at the moment of loss. The factor grid below maps what underwriters and brokers should be reviewing when sizing the limit against your rent roll.

Limit Adequacy

What Drives Your Loss of Rents Limit Adequacy

The premium is small. The limit-adequacy question is the one that decides whether the policy responds at the moment of loss. Here's what should be reviewed when sizing the limit against your rent roll.

| Rating Factor | Impact on Premium | |

|---|---|---|

| Rent roll relative to building value | SignificantHigh-rent / low-value properties carry outsized exposure relative to structural rebuild cost | |

| Lease term length / tenant credit | NotableLong-term tenant with good credit vs short-term turnover changes recovery timeline | |

| Typical repair timeline for property class | SignificantFrame strip mall repairs faster than masonry; restaurant kitchens slower than office | |

| Vacancy history | NotableVacant buildings rebuild slower; vacancy endorsement coordination matters | |

| Multi-tenant vs single-tenant exposure | SignificantMulti-tenant losses can stack across units in a single event | |

| Restaurant or higher-risk tenant inclusion | SignificantCooking operations dramatically increase fire frequency and repair-cycle length | |

| Wind / flood / coastal zone exposure | CriticalDisaster losses can run 12+ months; standard 12-month limit may be inadequate |

The limit needs to be reviewed annually against the actual rent roll, not the rent roll from when the policy was originally bound. Rent increases that the landlord captured years ago often don't show up on the policy until someone runs the review.

A few notes on how to read the table. The rent-roll-to-building-value ratio matters because high-rent / low-value properties (think restaurant tenant in a small building) carry outsized loss-of-rents exposure relative to the structural rebuild cost. Restaurant tenant inclusion is the single biggest premium-and-adequacy driver because cooking operations dramatically increase fire frequency — see our restaurant insurance guide for the tenant-side detail.

Before the next renewal

Most landlords set their loss-of-rents limit once and never review it against current rent rolls.

We pull your current declarations, confirm your loss-of-rents limit reflects current gross rent, and walk through what 12 months actually means when the repair cycle runs long.

“Loss of rents coverage is the single best premium-to-risk ratio in commercial insurance. When a tenant space goes dark, the mortgage doesn't pause. The policy that fills that gap costs less than the first month of lost rent.”

— Bobby Friel · Partner, Direct Insurance Services

Set on Autopilot vs. Set Right

The boards and landlords that get blindsided at the moment of loss are the ones whose loss-of-rents limit hasn't been touched since the original bind. The ones who don't are running a disciplined annual review. Five places where that discipline shows up:

Set on Autopilot

- ×Limit set years ago, never updated after rent increases

- ×4-6 month limit on 7-12 month repair cycles

- ×Vacancy gap unaddressed

- ×Tenant business income confused with landlord rental income

- ×No annual review against current rent roll

Set Right

- ✓12-month limit at current gross rent

- ✓Annual review against rent roll

- ✓Vacancy endorsement layered when needed

- ✓Landlord loss of rents distinguished from tenant business income in the lease

- ✓Replacement cost appraisal aligned with loss-of-rents adequacy

Building Owner Scenario

OPERATOR SCENARIO

Scenario

Imagine your strip-mall property loses one tenant to a kitchen fire and another to a burst pipe in the same calendar year. The structural repairs are covered. The 8 months of combined lost rent are partially uncovered because your loss-of-rents limit was set against rents that haven't been raised in three years.

What we did

What changes for the mortgage on that property if 8 months of rental income vanish and the loss-of-rents limit only covers 4? Where does the gap come out of?

🎯 The Outcome

Could a limit that hasn't been touched since the last carrier change already be the cash-flow hole that surfaces the next time a covered loss hits the property?

Common Mistakes Landlords Make

Not carrying it at all. This is the most common mistake. Many landlords buy a basic property policy that covers the building but doesn't include loss of rents. They don't realize the gap until a claim happens.

Setting the limit too low. If your space rents for $10,000/month and you only carry $48,000 in loss of rents (4.8 months), but the repair takes 7 months, you're covering the last 2+ months yourself. The general guideline is 12 months of gross rent at current values.

Forgetting to update the limit after rent increases. You raised rent from $5,000 to $7,500/month two years ago, but your loss of rents limit still reflects the old rent. If a claim happens, you'll be reimbursed based on the old number unless the policy was updated. Annual review against the current rent roll catches this drift before it becomes a claim-time problem.

Confusing loss of rents with tenant's business income. Your loss of rents coverage protects YOUR rental income. It doesn't cover your tenant's lost business revenue — they need their own business income coverage on their commercial policy. The lease should require it. If you have restaurant tenants, they should carry restaurant insurance that includes their own business income coverage. And if your building has an HOA association managing shared structures, coordinate your commercial landlord policy with the HOA master policy to avoid gaps.

The Landlord Insurance Gaps Guide covers more blind spots we see regularly.

FAQ

How is loss of rents different from my tenant's business interruption coverage?

Loss of rents protects your rental income as the landlord. Business interruption protects your tenant's business revenue. These are two separate policies covering two separate exposures — your loss of rents reimburses the rent the tenant would have paid you, the tenant's business interruption reimburses the gross sales the tenant would have generated. The lease should require the tenant to carry their own business interruption coverage; that requirement doesn't replace your need for landlord loss of rents.

How much loss of rents coverage do I actually need?

The general guideline is 12 months of current gross rent across all units. Most repair cycles resolve in 2-6 months, but major losses (kitchen fire, structural water damage, hurricane damage) can run 7-12+ months. Setting the limit at 12 months of current rent gives the coverage headroom for the worst-case repair timeline. The limit needs to be reviewed annually against the actual rent roll, not the rent roll from when the policy was originally bound.

What's the difference between actual loss sustained and a fixed monthly limit?

Actual loss sustained pays whatever your real lost rental income is, up to the policy aggregate. Fixed monthly limit caps the monthly payout regardless of actual loss. Actual loss sustained gives more flexibility but requires good documentation; fixed monthly limit is simpler but caps payouts when actual losses run higher. Most modern commercial landlord forms write actual loss sustained as the default.

Does loss of rents cover vacant space waiting for the next tenant?

No. Loss of rents covers rental income lost because of a covered physical loss to the property (fire, water damage, wind, vandalism). It doesn't cover ordinary vacancy between tenants. For ordinary vacancy, the underlying property policy's vacancy provision is what triggers — and that's a separate conversation (see our commercial landlord insurance guide for the vacancy exclusion detail).

The Bottom Line

The smallest line on a commercial landlord policy is the one most landlords get wrong. Loss of rents costs less than the first month of lost rent — and only protects you if the limit reflects today's rent roll, not the rent roll from the last time anyone reviewed the policy.

Loss of rents is just one part of a complete commercial landlord insurance program — for the full picture (building coverage, premises liability, vacancy endorsement, umbrella stack), read the building owner guide. When a covered loss happens and you need rebuild work done, make sure your contractor carries proper insurance for tenant improvement and rebuild projects to avoid additional liability exposure. If you have restaurant tenants, coordinate your landlord policy with their restaurant insurance, especially their own business income coverage. And if your building sits inside a mixed-use development with an HOA, the HOA master policy covers shared structures but doesn't replace your individual landlord coverage.

Commercial Landlord Insurance rates vary by state — California and Colorado have different premium structures. Check our state-specific commercial insurance guides for details. And if you're looking to acquire additional properties or refinance, commercial real estate loans and building owner financing can help you move quickly.

Use our commercial landlord risk calculator to see where your factors land, then we'll review your current loss-of-rents limit against your actual rent roll before the next renewal.

The landlord's question

Not "should I carry loss of rents." The right question is "does the limit on my current policy actually reflect today's rent roll, and how many months of repair will the policy cover before the gap starts coming out of cash flow?" The premium is small. The limit decision is the line that matters.

About the Author

Bobby Friel

Partner, Direct Insurance Services

Bobby Friel is a partner at Direct Insurance Services, where Patrick Henigan and the licensed team handle all quoting, policy reviews, and binding. Bobby runs the commercial division's marketing, content, and client outreach — helping contractors, HOA boards, restaurant owners, and commercial landlords across 29 states find the right coverage through Insurance Service 365.

Related Coverage

Explore Related Coverage Options

🏠 The Complete Commercial Landlord Insurance Guide 2026

What every building owner needs to know about lessors risk, loss of rents, vacancy exclusions, and the coverage gaps that leave landlords exposed.

Read the Free Guide →

Ready When You Are

Ready When You Are

No pressure. No obligation. Just real quotes from 30+ carriers, reviewed on video so you understand exactly what you're buying.

Takes ~2 minutes · Contract review included · Video walkthrough on every option