Certificate of Insurance (COI): What It Is, What's On It

Last updated: May 26, 2026

Key Takeaway

A Certificate of Insurance (COI) is a one-page document that proves you have active insurance coverage. It’s not the policy itself — it’s proof that the policy exists. Every contractor needs COIs because GCs, property managers, and clients require them before you can start work. Getting rejected for a bad or expired COI costs you jobs and money.

What is a Certificate of Insurance (COI)?

A Certificate of Insurance is a standardized one-page document (ACORD form) that summarizes your insurance coverage, including policy types, limits, effective dates, and named insureds. It proves to third parties that you carry active insurance. It is NOT the policy itself and cannot modify or extend your actual coverage.

FOR CONTRACTORS

The certificate isn't the policy. That gap is where contractors lose jobs.

A COI is a snapshot of a policy at one moment. If the underlying policy doesn't carry the endorsements the certificate references, the certificate is a misrepresentation — and the gap surfaces at audit, at compliance check, or at the claim. The fix lives in the policy, not the certificate.

Turned Away at the Job Site

A plumber shows up to a commercial job site ready to start a three-week project. The general contractor's site manager meets him at the gate and asks for the Certificate of Insurance. The plumber pulls up the PDF on his phone — and the site manager points to the expiration date. The policy lapsed two weeks ago. He's told to leave and not come back until he has a current COI.

That scenario is more common than it should be. A COI is one of the simplest documents in contractor insurance — but the gap between "I have a certificate" and "I have current coverage with the endorsements the contract actually demands" is where contractors lose jobs, lose time, and lose money every week. The certificate isn't the policy. It's a snapshot of the policy at the moment the certificate was issued — and if the policy isn't right, the certificate doesn't make it right.

36K+

participating organizations across 100+ countries using ACORD standards — the COI is one of the most universally exchanged documents in commercial insurance

ACORD, organization profile, 2024

1,200+

standardized insurance transaction types maintained by ACORD across the industry — the COI sits inside a much larger standardized exchange

ACORD, data standards library

15.1%

share of construction and extraction workers operating as independent contractors — the highest rate of any major industry, driving daily COI verification at the job-site level

BLS Contingent Worker Survey, July 2023

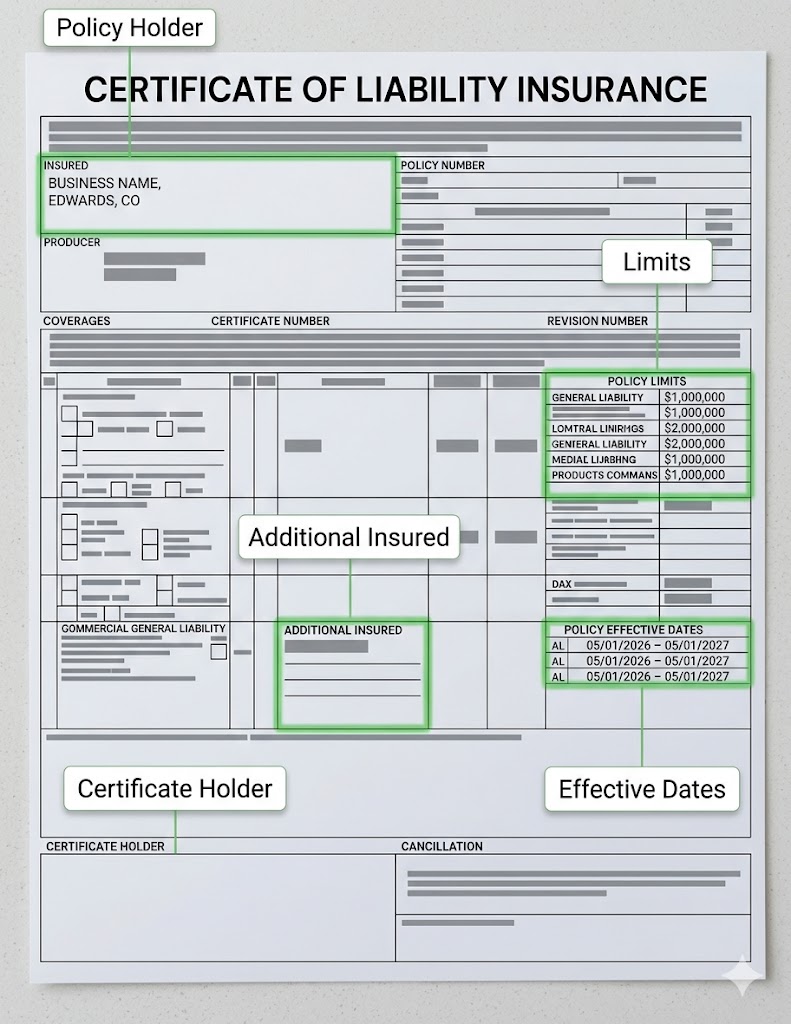

What's on a COI

A Certificate of Insurance is a one-page summary of your insurance coverage, issued on a standardized form called an ACORD 25. Its only purpose is to prove to a third party that an active insurance policy exists. It lists policy types, coverage limits, effective and expiration dates, and named insureds. It is not the policy itself — there's a disclaimer printed on the form that says exactly that. The COI is informational; the policy is the contract.

Every ACORD 25 contains the same fields, laid out in the same format. The grid below maps each field and what it represents.

01

🏷️Certificate Holder

The person or company who requested the certificate. Listed at the top of the ACORD 25. This field tells the carrier and the GC who is supposed to receive notifications about the policy. Names must match the contract exactly — compliance platforms flag mismatched entity names automatically.

02

🏢Insured (Your Business)

Your legal business name as it appears on your LLC or corporation documents, address, and contact information. This is the party the policy is issued to. Misalignment between business name and contract creates compliance rejections regardless of coverage quality.

03

📊Coverages and Limits

Each policy line gets its own row: GL, workers comp, commercial auto, umbrella, professional liability. For each, the certificate shows the carrier, policy number, effective date, expiration date, and the limit structure. GCs read this section against their contract requirements line by line.

04

📅Effective and Expiration Dates

The active policy window. A certificate showing dates that don't cover the full project timeline gets rejected — the GC won't accept a policy that expires before the work finishes. If the policy lapses mid-project, the certificate is no longer accurate even though it was correct when issued.

05

📝Description of Operations

The bottom field where the agent adds contract-specific notes — additional insured language, waiver of subrogation references, primary and non-contributory wording, project-specific details. This is the field where most "additional insured" claims on certificates exist purely as typed text without the actual policy endorsement behind them.

Think of it like a driver's license. The license proves authorization to drive; it's not the law that grants the right to drive. Similarly, the COI proves a policy exists; it's not the insurance contract itself. The downstream consequence: any field on the certificate that misrepresents the underlying policy is a problem that surfaces at audit, at compliance check, or at the claim — long after the certificate was issued.

What Each Customer Type Demands

Almost everyone a contractor works for will require a COI before work starts. What they require on it varies by customer type. The table below maps demand profiles by who's asking.

COI Requirements

What Each Customer Type Demands on the COI

Almost every commercial customer requires a COI before work starts — but what they demand on it varies. The grid below maps demand profiles by customer type so you can confirm your policy actually carries what the next contract is going to ask for.

| Rating Factor | Impact on Premium | |

|---|---|---|

| General contractors | CriticalHighest demands: $1M/$2M GL, WC, AI for ongoing + completed ops, waiver of subrogation, per-project aggregate | |

| Property managers | Significant$1M/$2M GL, WC if you have employees, AI naming property owner | |

| Government / municipal | Critical$1M/$2M or $2M/$4M GL, WC, AI, 30-day cancellation notice, umbrella often required | |

| Homeowners (direct hire) | Minor$500K–$1M GL, state-specific WC, proof of active coverage typically enough | |

| Commercial landlords | NotableAI naming property owner, waiver of subrogation, often per-location requirements | |

| HOA boards | NotableAI, WC even for solo contractors, often specific endorsements per CC&Rs |

The pattern: commercial customers (GCs, government, landlords, HOAs) demand specific endorsement language; homeowners typically don't. The endorsement stack on the policy determines which contracts you can actually clear compliance for — not the headline limit on the certificate.

General contractors and government customers are the most demanding — and for good reason. If your work causes damage or injury on their job site, they need to know your insurance will respond before theirs does. That's why they require not just proof of insurance, but specific endorsements like additional insured status and waiver of subrogation. Commercial landlords have similar requirements — if you're doing work on leased property, the landlord's lessors risk insurance policy often requires COIs from every contractor on site.

Before the next COI goes out

Most COIs that get rejected list endorsements that were never actually added to the policy.

We pull your policy form (not just the certificate), confirm whether the endorsements the GC is asking for are actually attached, and surface the gap before the certificate gets kicked back.

“You can't just type a name on a COI and call it an additional insured. The endorsement has to actually be added to the underlying policy. A COI that lists someone as an additional insured without the actual endorsement in place is misleading — and won't hold up if there's a claim.”

— Bobby Friel · Partner, Direct Insurance Services

On the Certificate vs. On the Policy

The additional insured endorsement is the most requested — and most misunderstood — part of the COI process. When a GC asks to be listed as an additional insured on your policy, they're asking for your insurance to extend coverage to them for claims arising from your work. That extension only exists if the underlying policy actually has the endorsement on it. A name typed on the certificate doesn't create the endorsement; it just notes that the endorsement should be there.

On the Certificate (what most agents send)

- ×Name typed in the certificate holder field

- ×AI box checked on the ACORD 25 form

- ×"Additional insured" noted in the Description of Operations

- ×Loose entity name match to the contract

- ×Standard form generated from a template, no contract review

On the Policy (what actually counts)

- ✓CG 20 10 + CG 20 37 endorsements actually attached to the policy form

- ✓Entity name matches the contract exactly — including LLC, Inc., commas

- ✓Ongoing AND completed operations AI both endorsed

- ✓Endorsement copies available on request for compliance audit

- ✓Contract reviewed before bind so the policy structure matches what the GC demands

Contractor Scenario

OPERATOR SCENARIO

Scenario

Imagine your GC's compliance platform just flagged your COI. The AI endorsement is shown on the certificate. The audit team is asking for a copy of the endorsement form attached to the policy. Your agent told you "additional insured is on the certificate" — they never actually endorsed the policy.

What we did

What happens if the GC's compliance team asks to see the CG 20 10 endorsement form itself — not the certificate? Who covers the loss if a claim hits while the AI shows on paper but doesn't exist on the policy?

🎯 The Outcome

Could the certificate you've been sending for two years already be the gap that voids your additional insured status when it actually matters?

For deeper detail on the rejection patterns this gap produces, see why your COI keeps getting rejected. For the speed conversation — and why same-day binding is the gap most rejected COIs come from — see why speed without review costs you jobs. The Contractor COI Checklist covers the endorsement language every commercial GC contract typically demands.

FAQ

Does a COI mean I'm actually covered, or just that I had coverage on the date it was issued?

The COI represents coverage at the moment it was issued. If the policy lapses, cancels, or gets restructured after the certificate goes out, the certificate doesn't update itself. That's why GCs check certificates against carrier records at compliance time — they want to verify the policy is still in force, not just that a certificate was issued at some point in the past.

What's the difference between an additional insured and a certificate holder?

Certificate holder means the GC receives a copy of the certificate and gets notified if the policy cancels. Additional insured means the GC is actually covered under your policy for claims arising from your work — your policy extends to defend and indemnify them. Certificate holder is informational. Additional insured is real coverage. Commercial GCs typically want both.

How long is a COI valid for?

The certificate is valid until the policy expiration date shown on it, or until the policy is cancelled — whichever comes first. Most commercial policies run 12 months, so most COIs are valid for 12 months from the effective date. If the policy renews, the GC typically asks for a new certificate reflecting the new effective and expiration dates.

What does CG 20 10 mean and why do GCs ask for it?

CG 20 10 is the ISO standard endorsement form that adds a third party as an additional insured for ongoing operations under a commercial general liability policy. CG 20 37 is the companion endorsement for completed operations. GCs ask for these specific form numbers because they want to verify the actual endorsement is attached to the policy — not just typed onto the certificate. The form number is the evidence; the typed name on the certificate is just the reflection.

The Bottom Line

A Certificate of Insurance is one page of paperwork. The policy behind it is what actually pays a claim. Most COI problems aren't about what's on the certificate — they're about what's not on the policy. The fix is reading the contract before binding and making sure the policy form actually carries the endorsements the certificate references.

If your certificates keep getting kicked back even when coverage is in force, the diagnosis lives at why your COI keeps getting rejected. For the speed side — and why same-day binding without contract review is the gap most rejected COIs come from — see why speed without review costs you jobs. State-specific requirements are at our state commercial insurance guides.

The fastest way to find out where your current setup stands? Use our contractor insurance risk calculator, then we'll review the contract, confirm the endorsements are actually on the policy, and walk through the gaps before the next COI request lands.

The contractor's question

Not "what's on my certificate." The right question is "what's actually endorsed on my policy form — and does it match what every GC contract I bid into next year is going to demand?" The certificate is the reflection. The policy is the substance.

About the Author

Bobby Friel

Partner, Direct Insurance Services

Bobby Friel is a partner at Direct Insurance Services, where Patrick Henigan and the licensed team handle all quoting, policy reviews, and binding. Bobby runs the commercial division's marketing, content, and client outreach — helping contractors, HOA boards, restaurant owners, and commercial landlords across 29 states find the right coverage through Insurance Service 365.

Related Coverage

Explore Related Coverage Options

🔨 The Complete Contractor Insurance Guide 2026

What every contractor needs to know about general liability, workers comp, commercial auto, tools coverage, and the COI requirements that kill jobs.

Read the Free Guide →

Ready When You Are

Ready When You Are

No pressure. No obligation. Just real quotes from 30+ carriers, reviewed on video so you understand exactly what you're buying.

Takes ~2 minutes · Contract review included · Video walkthrough on every option