Restaurant Insurance Cost 2026: 12 Factors That Move It

Last updated: May 26, 2026

Key Takeaway

Every online restaurant insurance calculator averages your reality into one number. That number is wrong for almost every restaurant it gets shown to. The 12 factors carriers actually rate against — cuisine type, prep method, liquor percentage, lease endorsement requirements, claims history — are operational details no calculator can know. The conversation worth having before the next renewal isn't about the average. It's about which factors are moving your specific quote and which ones your current agent isn't checking.

How much does restaurant insurance cost in 2026?

There is no honest single-number answer. A fine-dining restaurant in Chicago pays completely differently than a quick-service taco shop in Austin or a brewpub in Portland — and all three pay differently than what an online calculator predicts. The twelve factors below are what actually drive every restaurant insurance quote. What a specific restaurant pays is determined by how those factors stack up for the operation, which is why any quote worth trusting comes after a real conversation about cuisine, liquor percentage, lease endorsements, and claims history — not before.

FOR RESTAURANTS

You searched for a number. Every source gave you a different one.

Every online restaurant insurance calculator averages realities into one number. That number is wrong for almost every restaurant it gets shown to. The 12 factors carriers actually rate against are operational details no calculator can know — cuisine type, prep method, liquor percentage, lease endorsement requirements, claims history. The conversation worth having before the next renewal isn't about the average. It's about which of the 12 factors is moving your specific quote — and which ones your current agent isn't even checking.

You Searched for a Number. Every Source Gave You a Different One.

You searched for a number. We get it — trying to budget the next 12 months, compare a renewal quote, or figure out whether the number your current agent gave you is fair. Every online restaurant insurance calculator averages your reality into one number. That number is wrong for almost every restaurant it gets shown to.

The 12 factors carriers actually rate against are operational details no calculator can know — cuisine type, prep method, liquor percentage, lease endorsement requirements, claims history. The conversation worth having before the next renewal isn't about the average. It's about which factors are moving your specific quote, and which ones your current agent isn't even checking. For the lease-side detail that drives a meaningful share of restaurant premium variation, see liquor liability insurance and the alcohol exclusion every commercial GL writes.

1M+

restaurant locations in the U.S. — the universe where 12 factors decide whether the renewal matches the operation or misses by a year's worth of margin

National Restaurant Association, 2025 State of the Restaurant Industry

15.9M

total restaurant and foodservice employment in the U.S. by year-end 2025 — the workers comp exposure restaurant programs underwrite against

National Restaurant Association, 2025 State of the Restaurant Industry

$1.5T

projected U.S. restaurant industry sales in 2025 — the revenue base GL and property premiums scale against, and the margin pressure renewal increases hit hardest

National Restaurant Association, 2025 State of the Restaurant Industry

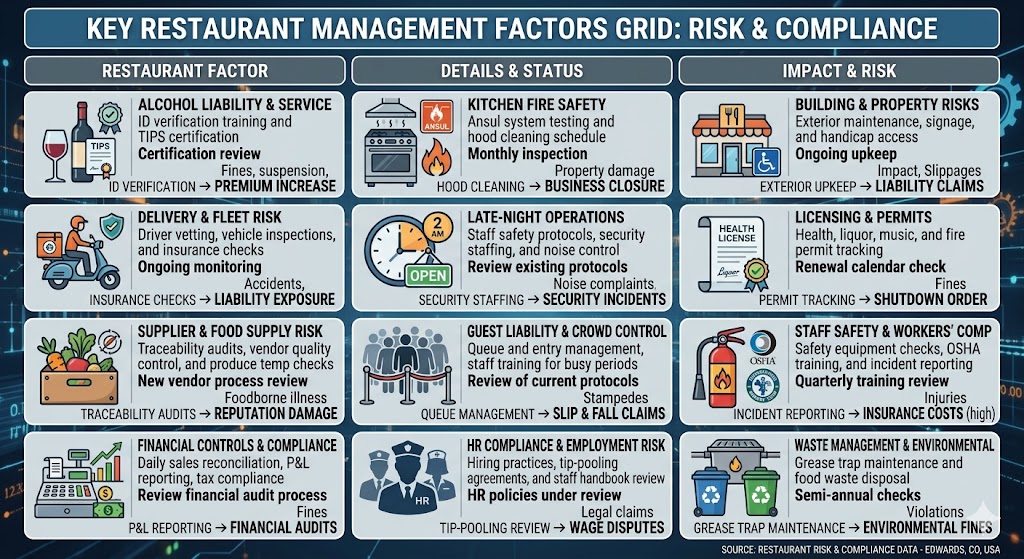

The 12 Factors That Move Every Restaurant Quote

Restaurant insurance pricing isn't random — it's calculated from twelve factors every underwriter looks at. The table below maps each factor with magnitude direction, roughly in order of how much each moves the premium.

Premium Drivers

What Drives Your Restaurant Insurance Premium

Restaurant insurance pricing depends on twelve factors specific to your operation. Here's what underwriters actually rate against — and where most online calculators get it wrong.

| Rating Factor | Impact on Premium | |

|---|---|---|

| Cuisine type and preparation methods | SignificantFryer, open flame, wok, charbroiler each carry different fire and grease exposure | |

| Annual revenue and seating capacity | SignificantGL and property scale with business size and shift volume | |

| Liquor sales percentage | CriticalThe single biggest lever; past 50% alcohol revenue, carrier appetite narrows | |

| State and jurisdiction | SignificantDram shop law, labor costs, litigation climate vary widely | |

| Delivery operations (in-house vs platform vs none) | NotableIn-house delivery adds hired and non-owned auto exposure | |

| Square footage and building age | NotableOlder buildings carry older electrical, plumbing, hood systems | |

| Claims history (3-5 years) | CriticalTwo slip-and-falls or a grease fire materially change renewal pricing | |

| Employee count and payroll | SignificantWC rated directly off payroll; headcount feeds GL exposure too | |

| Coverage limits required by lease | NotableMost leases demand $1M/$2M; mall and mixed-use require more | |

| Lease endorsement requirements (AI, WoS, PNC) | NotableMissing endorsements trigger lease-default notices and COI rejections | |

| Equipment value and kitchen installations | NotableProperty coverage rated on ranges, hoods, walk-ins, POS, smallwares | |

| Alcohol service hours and entertainment | CriticalLate-night service and entertainment license narrow carrier appetite |

No single factor decides the premium. The combination — and especially how cuisine type interacts with liquor percentage and lease endorsement requirements — is what determines whether the renewal matches the operation or misses it by a year's worth of margin.

A few notes on how to read the table. Cuisine type and prep method drive property rating more than overall revenue — a sushi bar prepping cold dishes prices very differently than a Korean BBQ spot with tabletop grilling or a southern fried chicken concept running banks of deep fryers. Liquor sales percentage is the single biggest lever on the total package; past 50% alcohol revenue, some carriers won't write the account at all. Lease endorsement requirements (additional insured, waiver of subrogation, primary and non-contributory) add premium and trigger lease-default notices when missing.

The Lines Every Restaurant Carries

A restaurant insurance program is rarely one policy. It's a stack of coverage lines stacked together — each addressing a different exposure, each priced separately, each tied to specific operational realities. The card grid below maps the lines.

01

⚖️General Liability

Covers customer injuries and property damage — someone slips on a wet floor, a server drops a tray, a customer has a severe allergic reaction. Most restaurants carry $1M per occurrence / $2M aggregate. Every commercial GL carries an alcohol exclusion by default, which is why liquor liability is a separate line.

02

🏢Property Insurance

Covers the building (if you own it), equipment, furniture, inventory, and business income if you're forced to close after a covered loss. A kitchen fire that shuts you down for two months doesn't just cost repair money — it costs revenue. Business income coverage is critical and often undervalued.

03

🍷Liquor Liability

Fills the alcohol exclusion every commercial GL writes by default. Covers bodily injury and property damage from intoxicated patrons, assault and battery claims with alcohol as a contributing factor, and dram shop liability under state law. Required for any restaurant that serves alcohol — even just beer and wine.

04

👷Workers Compensation

Covers employee injuries. Kitchen burns, knife cuts, slip-and-falls — restaurants have some of the highest injury rates of any industry. Rated directly off payroll and your state's classification rates. Required in nearly every state once you have employees.

05

🔧Equipment Breakdown

Covers mechanical failure of ovens, refrigeration, HVAC, ice machines, and other essential equipment. When a walk-in cooler dies on a Friday night and you lose inventory, equipment breakdown pays for the repair and the spoiled food. A small premium add-on with outsized claim utility.

06

⏸️Business Interruption

Replaces lost revenue when a covered loss forces the restaurant to close. Bundled with property in most BOPs, but the limit and the waiting period both need to be calibrated to the operation. A kitchen fire that shuts down a full-service restaurant for two months can erase the entire year's margin without it.

The most consequential line for restaurants that serve alcohol is liquor liability — every commercial GL carries an alcohol exclusion by default, and liquor liability is the policy that fills the gap. See liquor liability insurance: the hole in your restaurant GL for the deeper detail on when it triggers, what it covers, and what to verify before bind. For restaurants operating in leased commercial space, the landlord's lease endorsement requirements add premium and trigger lease-default exposure when missing — see commercial landlord insurance for the building-owner side of that conversation.

Before the next renewal

Most restaurant policies are bound against an estimate, not the operation.

We pull your current declarations, confirm your cuisine class, liquor percentage, and lease endorsement requirements are rated correctly, and walk through what's actually moving your premium.

“Every restaurant cost calculator online works by averaging realities into one number. That number is wrong for almost every restaurant it gets shown to. The questions worth asking are about your cuisine, your liquor percentage, and your lease — not about averages.”

— Bobby Friel · Partner, Direct Insurance Services

What the Online Calculator Misses

Every restaurant insurance calculator averages five generic assumptions into one number. The underwriter who actually writes the policy rates against ten or more specific operational details. Five places where that gap shows up:

What the Online Calculator Misses

- ×Generic cuisine bucket — sushi, BBQ, fried chicken all rated the same

- ×Single liquor % assumption regardless of actual sales mix

- ×Single state factor without dram shop law specificity

- ×No lease endorsement review (AI, WoS, PNC missing)

- ×Claims-clean assumption regardless of actual loss runs

What the Underwriter Actually Rates

- ✓Actual cuisine class with prep-method specifics (fryer, open flame, wok)

- ✓Real liquor percentage by sales mix and service hours

- ✓State-specific rate filings and dram shop law severity

- ✓Lease endorsement requirements (AI, WoS, PNC, project-specific)

- ✓Full claims history (3-5 year loss runs)

Restaurant Scenario

OPERATOR SCENARIO

Scenario

Imagine you just got the renewal quote on your full-service restaurant. The premium came back meaningfully higher than last year. The agent says it's because of "industry hardening." You can either eat the increase out of margin, raise menu prices, or cut shifts. None of those feel right.

What we did

What changes for your margin if your current agent never re-ran your lease endorsement stack against the current contract and the renewal carries endorsements you don't actually need?

🎯 The Outcome

Could the "industry hardening" increase already be the gap between what your policy is rated against and what your operation actually requires?

FAQ

Why don't you just tell me what restaurant insurance costs?

Because no honest answer fits in a single number. A steakhouse in Dallas with full liquor pays a completely different premium than a neighborhood pizzeria in Phoenix with limited beer-and-wine service — and both pay differently than a food truck in Austin with one vehicle and no seating. Every cost calculator online works by averaging those realities into one number. That number is wrong for almost every restaurant it gets shown to. What's on this page instead: the twelve factors that actually move every restaurant quote, what each factor actually does to your number, and the questions to ask your agent so your quote matches what you'll actually pay.

How does liquor liability affect my total restaurant insurance cost?

Liquor liability is a separate policy from your GL because every commercial GL writes an alcohol exclusion by default. The premium scales with your alcohol revenue percentage, your service hours, and your state's dram shop law. Past 50% alcohol revenue, carrier appetite narrows significantly. See liquor liability insurance for the full conversation on what it covers and what to verify.

What's the difference between business income and equipment breakdown?

Business income coverage replaces lost revenue when a covered loss forces the restaurant to close — a kitchen fire that shuts you down for two months doesn't just cost repair money, it costs the revenue those two months would have generated. Equipment breakdown covers mechanical failure of essential equipment — when a walk-in cooler dies on a Friday night and you lose inventory, equipment breakdown pays for the repair and the spoiled food. Both lines are typically undervalued on standard restaurant programs.

Does my landlord's lease actually require specific insurance endorsements?

Almost certainly yes. Most restaurant leases name the landlord as additional insured, require a waiver of subrogation, and some require primary and non-contributory language and specific ISO forms. These endorsements add premium — and if they're missing from your policy when the landlord audits your COI, you get a lease default notice. The lease should be reviewed before binding the policy, not after the COI gets rejected.

The Bottom Line

You've seen the twelve factors. The question worth asking isn't "what does restaurant insurance cost" — it's "which of those twelve factors are costing me money I don't need to spend, and which are under-covered on my current policy?"

That's the conversation that actually saves restaurants money. Not the generic number. The specific gaps and overages hiding in the current coverage. If your restaurant serves alcohol, liquor liability insurance is usually its own policy — different rating logic than your GL, and the policy that fills the alcohol exclusion every commercial GL writes by default. And for restaurants operating in leased commercial space, the landlord's commercial landlord insurance requirements often dictate which endorsements your policy needs to carry.

Check our Restaurant Coverage Checklist before the next renewal, and if you're building out a new location, make sure your contractor carries proper insurance for the construction phase. Restaurants in mixed-use buildings with HOA associations have additional coordination requirements. Need help with startup costs or the insurance deposit? Restaurant equipment loans and startup financing can help.

The fastest way to find out where you stand? Use our restaurant insurance risk calculator to see which of the twelve factors are working for you and which are working against you. Then we'll compare 30+ carriers and walk through real coverage options for your specific restaurant — not a budget estimate that won't survive the next renewal.

The restaurant operator's question

Not "what does restaurant insurance cost." The right question is "which of the twelve factors is moving my specific quote, and which ones is my current agent not even checking?" The headline premium is the surface. The cuisine class, liquor percentage, and lease endorsement stack are the story.

About the Author

Bobby Friel

Partner, Direct Insurance Services

Bobby Friel is a partner at Direct Insurance Services, where Patrick Henigan and the licensed team handle all quoting, policy reviews, and binding. Bobby runs the commercial division's marketing, content, and client outreach — helping contractors, HOA boards, restaurant owners, and commercial landlords across 29 states find the right coverage through Insurance Service 365.

Related Coverage

Explore Related Coverage Options

🍽️ The Complete Restaurant Insurance Guide 2026

What every restaurant owner needs to know about liquor liability, business interruption, equipment breakdown, and the lease requirements that blindside operators.

Read the Free Guide →

Ready When You Are

Ready When You Are

No pressure. No obligation. Just real quotes from 30+ carriers, reviewed on video so you understand exactly what you're buying.

Takes ~2 minutes · Contract review included · Video walkthrough on every option