GL Insurance for Contractors: Why Completed Ops Matters

Last updated: May 26, 2026

Key Takeaway

General liability insurance for contractors covers third-party bodily injury, property damage, and — critically — completed operations claims that can surface months or years after a job closes. The single biggest GL gap most contractors carry is a policy that excludes completed operations. The premium savings vanish the first time a job comes back to haunt the policy.

What does general liability insurance cover for contractors?

GL covers three main areas: bodily injury to third parties (a client trips over your equipment), property damage (you accidentally drill through a water line), and completed operations (a claim arising from work you finished weeks or months ago). It does NOT cover employee injuries (that's workers comp), your vehicles (that's commercial auto), or your own tools and equipment (that's inland marine).

FOR CONTRACTORS

A job you finished last year can still be your liability this year.

The single most consequential decision on a contractor GL policy is whether completed operations is on or off the form. Two policies can quote at similar premium and look identical on a certificate, but respond very differently when a claim arrives a year after the job closed. The gap surfaces at the worst possible moment — when a homeowner attorney is already on the phone.

The single most expensive gap in contractor general liability insurance isn't a low limit or a missing endorsement. It's a policy that excludes completed operations — the coverage that responds when a job comes back to haunt the policy months or years after you walked off the site.

The premium savings on a "premises and operations only" GL policy look attractive on the bind quote. They vanish the first time an electrical fault, a plumbing fitting, or a flashing detail surfaces a claim long after the job closed. The policy that was active during the work no longer responds. The current policy excludes the work.

This page walks through what GL actually covers, what it doesn't, and the 12 factors that move every contractor GL quote — with a focus on the completed operations conversation that should be happening before bind, not after the lawsuit.

8.3M

U.S. construction payroll employment as of August 2024 — every trade rated by its own class code, and every trade exposed to completed-operations claims long after the work closes

BLS Current Employment Statistics, August 2024

2.3

nonfatal workplace injuries per 100 full-time construction workers in 2023 — the third-party injury and property damage frequency carriers price GL against

BLS Survey of Occupational Injuries and Illnesses, 2023

9.2

fatal injuries per 100,000 full-time construction workers in 2024 — the tail-risk reality that shapes carrier appetite and rates on GL completed operations

BLS Census of Fatal Occupational Injuries, 2024

Why Completed Operations Matters

Completed operations coverage is included in most standard GL policies — but not all. Budget carriers and online quote platforms sometimes sell premises-and-operations-only policies that specifically exclude completed operations to keep the headline premium low. Below the headline, the math gets ugly.

For most contractors, the biggest risks don't happen while you're on the job — they happen after you leave. An electrician who wires a panel incorrectly might not see a problem for a year — until an arc fault starts a fire. A plumber whose fitting fails might not hear about it until water damage shows up behind a wall. A roofer whose flashing wasn't sealed right might not get a call until the next storm season. These are all completed operations claims. They're often the most expensive claims contractors face because the damage has time to compound before anyone notices.

When we quote contractors in California, Texas, Colorado, or Ohio, completed operations is always included. It's not optional from where we sit. If your current policy doesn't include it, that's the first conversation to have before the next bid window opens.

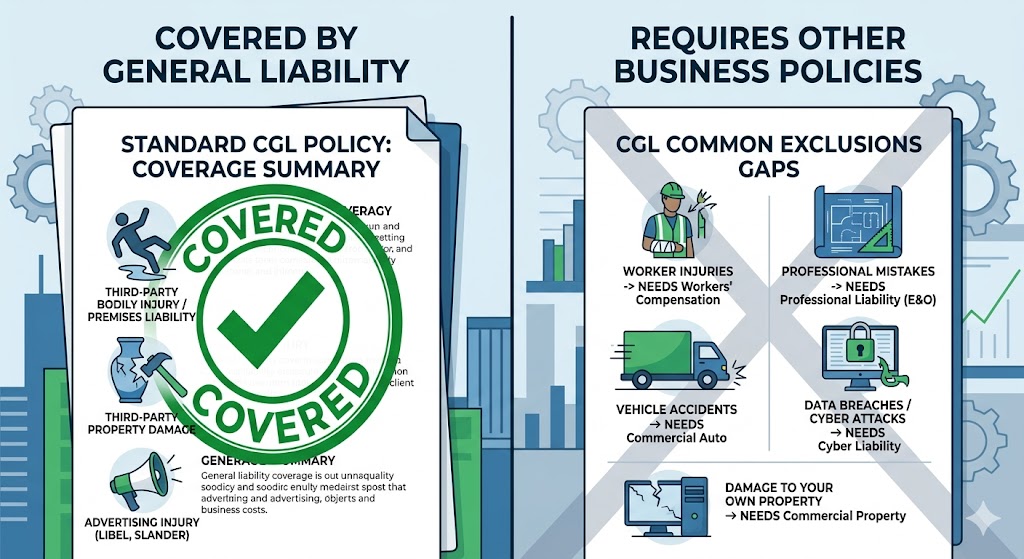

What GL Covers and What It Doesn't

General liability insurance for contractors covers three main categories of risk: third-party bodily injury, third-party property damage, and completed operations. It also covers legal defense costs — attorney fees, court costs, settlements — even when claims turn out to be frivolous. The factor grid below lays out the boundary between what GL handles and what it explicitly doesn't.

01

🤕Third-Party Bodily Injury

Covered. If a homeowner, passerby, or anyone who isn't your employee gets hurt because of your work or your presence on a jobsite, GL pays medical bills and legal defense.

02

🏚️Third-Party Property Damage

Covered. If your work damages someone else's property — buried gas line, dented client car, flooded basement from a pressure-test failure — GL handles repair or replacement.

03

⏳Completed Operations

Covered when on the policy form; excluded on premises-and-operations-only policies. Claims that arise after you've finished — faulty wiring fire, failed plumbing fitting, roof leak the next spring.

04

⚖️Legal Defense Costs

Covered, typically outside the policy limit on standard contractor GL forms. Attorney fees, court costs, settlements — even when the claim is ultimately frivolous.

05

🚫Employee Injuries

Not covered. Workers comp handles employee injuries. See our guide on contractor workers comp cost for that side of the program.

06

🚫Your Vehicles, Tools, Design Errors

Not covered. Vehicles need commercial auto. Tools need inland marine. Design errors need professional liability. GL covers third-party exposure to your work — not your own assets or your own design decisions.

Employee injuries are workers comp, not GL — see our guide on contractor workers comp cost for that side. Your vehicles are commercial auto. Your tools are inland marine. Your design errors (if you're a design-build contractor) are professional liability. And no policy of any kind covers intentional damage or fraud. The lines look obvious on paper; they get blurred in real claims, which is why the policy review before bind matters more than the headline premium.

The 12 Factors That Move GL Premium

GL pricing is rated against a defined set of factors — trade classification, revenue, claims history, completed-ops exposure, contract requirements, state, and the rest of the table below. The same contractor will get materially different quotes depending on which factors land harder and which carriers see the trade most favorably.

Premium Drivers

What Drives Your Contractor GL Premium

GL pricing depends on a stack of factors specific to your trade and your project history. Here's what underwriters actually rate against — and where the completed-operations question shows up.

| Rating Factor | Impact on Premium | |

|---|---|---|

| Trade classification | CriticalThe starting point — roofing, masonry, electrical, plumbing all rate very differently | |

| Annual revenue | CriticalGL scales directly with revenue and project volume | |

| Completed operations exposure | CriticalThe single biggest GL gap — included or excluded changes everything | |

| Claims history (last 5 years) | CriticalFrequency and severity both weighted; completed-ops claims hit hardest | |

| Coverage limits required by contract | SignificantStandard $1M/$2M vs $2M/$4M vs umbrella stacks layer on top | |

| Additional insured / waiver of subrogation endorsements | SignificantGC contract language drives endorsement stack and premium | |

| State and jurisdiction | NotableLitigation climate, statute of repose, and rate filings vary widely | |

| Subcontractor controls and COI verification | NotableUninsured subs roll into your audit; downstream exposure to your GL | |

| Safety program and OSHA record | NotableDocumented program earns carrier credit on the GL side | |

| Deductible / SIR selection | MinorHigher deductibles reduce premium but increase cash flow exposure | |

| Years in business | MinorMature operations earn carrier credit; new ventures price harder | |

| Project mix (residential vs commercial vs industrial) | NotableAggregate-erosion risk highest in high-volume residential |

No single factor decides the premium. The combination — and especially whether the policy includes completed operations or excludes it — is what determines whether the policy still defends you when a job comes back a year after the work closed.

For deeper detail on how GL stacks with workers comp and the rest of a contractor program, see our complete contractor insurance cost breakdown. For the workers comp discipline specifically, see contractor workers comp cost. And if your COIs keep getting rejected by GCs, that's typically an endorsement-stack problem on the GL policy, not a paperwork problem.

Walk through your current GL form

Want to know if your current GL has completed operations coverage included?

We pull your policy form (not just the certificate), confirm whether completed operations is on or off, and walk you through every gap before the next GC contract demands a new endorsement.

“For most contractors, the biggest risks don't happen while you're on the job — they happen after you leave.”

— Bobby Friel · Partner, Direct Insurance Services

Premises Only vs. Completed Ops Coverage

The single most consequential decision on a contractor GL policy is whether completed operations is on or off. Two policies can quote at similar premium and look identical on a certificate, but respond very differently when a claim arrives a year after the job closed. The difference shows up in a handful of places:

GL Premises and Operations Only

- ×Post-job claims denied — coverage stopped the moment you walked off the site

- ×GC contract requirements typically unmet — most GCs demand products/completed operations on the COI

- ×Personal exposure on settlement when the policy doesn't respond

- ×No defense costs covered once the project closed

- ×Premium savings vanish the first time a job comes back

GL with Completed Operations

- ✓Post-job claims defended through the statute of repose in your state

- ✓Full GC contract compliance — products/completed operations endorsement on the COI

- ✓Business-shielded settlement exposure under occurrence-form coverage

- ✓Defense costs covered throughout the tail period, typically outside the limit

- ✓Policy structure matches what every legitimate commercial contract demands

Contractor Scenario

OPERATOR SCENARIO

Scenario

Imagine you finished a kitchen remodel 14 months ago. Last week the homeowner discovered water damage tracing back to the work — a pinhole leak in the plumbing your crew installed. They're calling their attorney. You're getting served.

What we did

If your GL policy didn't have completed operations coverage on it when that job closed, who pays the defense costs now? The policy that was active during the work no longer covers it. The current policy excludes it.

🎯 The Outcome

Could a job you finished last year still be your liability this year — and your personal liability if the policy structure was wrong from day one?

How to Buy the Right GL Policy

Limits, endorsements, completed operations, and the policy form itself all matter more than the headline premium. What the policy review process should walk through:

Confirm completed operations is included. Ask specifically, and confirm by reading the policy form — not the certificate. "Premises and operations only" is the budget-carrier flag to watch for.

Match limits to contract requirements. Most GCs require $1M per occurrence / $2M aggregate as a baseline. Larger commercial projects sometimes demand $2M/$4M or an umbrella sitting above the GL. Limits language matters more than the headline number — read the GC contract before binding the limit.

Check additional insured and waiver of subrogation endorsements. Most GCs require both. Some carriers include them automatically; others charge extra. The Contractor COI Checklist covers exactly what to look for.

Get the certificates right the first time. A COI that doesn't match the contract requirements gets rejected — and the bid window doesn't pause for the correction. We turn around COIs quickly and format them correctly for the GC asking.

Shop the market every renewal. GL pricing for the same contractor can vary meaningfully between carriers depending on appetite for the trade, state, and loss history. Use our Contractor Insurance Risk Calculator to get a starting view, or go straight to a full quote. If the upfront premium deposit creates cash flow strain, business financing for contractors can cover it.

FAQ

What's the difference between GL with completed operations and an OCIP or CCIP?

GL with completed operations is your own policy that responds to claims arising from your work, including after the job closes. An OCIP (Owner-Controlled Insurance Program) or CCIP (Contractor-Controlled Insurance Program) is project-specific coverage that the project owner or general contractor places to cover everyone on a specific job. OCIP/CCIP typically replaces your GL for that one project only — but your own GL still needs to be in force for every other job you run.

Do I need GL if I already have workers comp?

Yes. Workers comp covers your employees' injuries. GL covers third-party injuries and property damage — homeowners, passersby, GCs, other trades on the jobsite, anyone who isn't your employee. They're separate policies covering separate exposures, and most GC contracts require both.

What does per-occurrence vs. aggregate actually mean for my business?

Per-occurrence is the maximum the policy pays for any single claim. Aggregate is the maximum the policy pays for all claims combined during the policy period. The standard $1M/$2M setup means $1M per claim, $2M total across the policy year. If you're running high-volume residential work with many active jobs at once, the aggregate is what runs out first — and once it's exhausted, the policy doesn't respond again until renewal.

When does my GL policy stop covering work I finished a year ago?

That depends on whether completed operations is included and whether your policy is occurrence-form or claims-made. Most contractor GL is occurrence-form with completed operations included — meaning the policy in force when the work was done covers the claim, even if the claim arrives years later. If your current policy is premises-and-operations-only, coverage stopped the moment you walked off the job. The statute of repose in your state sets the outer limit on how long after a job a completed operations claim can be filed.

The Bottom Line

Completed operations coverage isn't optional — it's the difference between a denied claim and a defended one when a job comes back to haunt you a year after you walked off the site. The premium savings on a premises-and-operations-only policy vanish the first time the work comes back. The endorsement stack on the COI matters more than the headline premium on the dec page.

GL isn't just for contractors — restaurants need general liability insurance too, and so do HOA boards for their common areas. If you work across multiple industries, check our state-specific commercial insurance guides for requirements in your area. And the broader workers comp picture for contractor crews lives at contractor workers comp cost.

The fastest way to find out where you stand? Use our contractor insurance risk calculator to see which of the twelve factors are working for you and which are working against you. It takes about two minutes. Then we'll compare 30+ carriers and walk through real GL options for your specific trade — with completed operations included as a baseline, not an upcharge.

The contractor's question

Not "what does GL cost." The right question is "does my current policy form actually include completed operations — and would it defend me if a job from last year comes back this year?" The certificate doesn't answer that. The policy form does.

About the Author

Bobby Friel

Partner, Direct Insurance Services

Bobby Friel is a partner at Direct Insurance Services, where Patrick Henigan and the licensed team handle all quoting, policy reviews, and binding. Bobby runs the commercial division's marketing, content, and client outreach — helping contractors, HOA boards, restaurant owners, and commercial landlords across 29 states find the right coverage through Insurance Service 365.

Related Coverage

Explore Related Coverage Options

🔨 The Complete Contractor Insurance Guide 2026

What every contractor needs to know about general liability, workers comp, commercial auto, tools coverage, and the COI requirements that kill jobs.

Read the Free Guide →

Ready When You Are

Ready When You Are

No pressure. No obligation. Just real quotes from 30+ carriers, reviewed on video so you understand exactly what you're buying.

Takes ~2 minutes · Contract review included · Video walkthrough on every option